2026 Tax Changes Explained in Plain English

As you have probably heard by now, tax rules have changed again for 2026. Some of the tax provisions that were set to expire after 2025 were updated and extended under the One Big Beautiful Bill. This quick overview covers the major changes that affect most individuals. As always, these rules apply to 2026 tax returns filed in 2027.

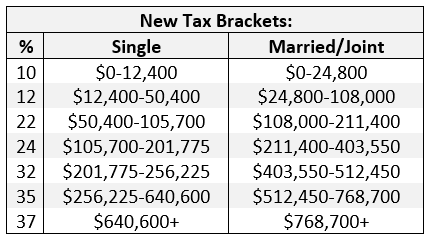

New Tax Brackets for 2026 (Federal Income Tax Rates)

Major Changes Most People Will Notice

• Standard Deduction: Increased again.

Single: $16,100 | Married Joint: $32,200 | Head of Household: $24,150

Most taxpayers will still take the standard deduction rather than itemize.

• Personal Exemptions: Still $0. This was made permanent under the newer law structure.

• AMT (Alternative Minimum Tax): Retained with higher exemption amounts. For 2026, the exemption is $90,100 (single) and $140,200 (joint), with phase-outs at higher income levels.

• Itemized Deductions: Limits on high-income taxpayers remain, although many taxpayers will see little impact if taking the standard deduction.

• Pass-Through Business Income: The 20% Qualified Business Income deduction continues, which is important for small business owners, independent agents, and consultants.

Big Beautiful Bill and Social Security Tax Changes - This is where many people are confused, so let’s make it simple. The law did not eliminate federal taxes on Social Security benefits. Social Security income can still be taxable depending on your total income.

What did change is a new temporary senior deduction. Individuals age 65 and older may qualify for an additional $6,000 deduction ($12,000 for qualifying married couples) from 2025 through 2028, subject to income limits.

What this really means is that some seniors may end up paying less or even no federal tax on their Social Security benefits, but this happens because of the extra deduction, not because Social Security itself became tax free.

These are only the highlights that affect most individuals. Tax law continues to evolve, and even small changes in income or deductions can change your outcome. Take time to review your situation with a qualified advisor so you can make smart moves before filing season. This summary is meant to keep you informed, not replace personal tax advice.